VBA input box method

A sequence of input boxes w/ the Black-Scholes model

There are five parameters to the Black-Scholes pricing model for an option on a non dividend paying stock. This module shows how a series of input boxes can be used to gather the values of these five parameters from the user. Assign the values to variables, then return the option price with a list of inputs to the user with a message box.

The input boxes use the VBA InputBox method, and are presented in the form of a wizard - each box is Step x of 5. Step 1 for the Stock price is shown in figure 1.

The VBA code for the input box sequence is shown in code window 1.

The VBA code

To allow easy testing of the box sequence, the user is able to allow default values in each box by setting the switch in line 9. TRUE displays default values, FALSE disables the default value feature. The CANCEL buttons exits the procedure.

Code 1: Macro

BSCallOptBoxes displays a series of input boxes as a 5 step wizard. Allows optional default values - returns call price and parameters to a message box

Option Explicit

Option Base 1

'' ==============================================

Sub BSCallOptBoxes()

Dim Stock As Double, Exercise As Double, Rate As Double, Sigma As Double, Time As Double

Dim BSCallOpt As Double

Dim D(5) As String

Dim Switch As Boolean: Switch = True '' <<<< Select: TRUE for defaults, FALSE for no defaults (blank)

If Switch Then D(1) = 42: D(2) = 40: D(3) = 0.05: D(4) = 0.2: D(5) = 0.5

Stock = Application.InputBox(Prompt:="Enter the Stock Price", _

Title:="xlf Option Pricer - Step 1 of 5", _

Default:=D(1), _

Type:=1)

If Stock = False Then Exit Sub

Exercise = Application.InputBox(Prompt:="Enter the Exercise Price", _

Title:="xlf Option Pricer - Step 2 of 5", _

Default:=D(2), _

Type:=1)

If Exercise = False Then Exit Sub

Rate = Application.InputBox(Prompt:="Enter the Risk Free rate as a decimal", _

Title:="xlf Option Pricer - Step 3 of 5", _

Default:=D(3), _

Type:=1)

If Rate = False Then Exit Sub

Sigma = Application.InputBox(Prompt:="Enter the Stock volatility as a decimal", _

Title:="xlf Option Pricer - Step 4 of 5", _

Default:=D(4), _

Type:=1)

If Sigma = False Then Exit Sub

Time = Application.InputBox(Prompt:="Enter the Time to Expiration, in years as a decimal", _

Title:="xlf Option Pricer - Step 5 of 5", _

Default:=D(5), _

Type:=1)

If Time = False Then Exit Sub

BSCallOpt = BSCall(Stock, Exercise, Rate, Sigma, Time)

MsgBox "Theoretical price of call: " & Format(BSCallOpt, "$#,##0.0000") & vbNewLine _

& "====================================" & vbNewLine _

& "With values - " & vbNewLine & vbNewLine _

& "Stock price: " & Format(Stock, "Currency") & vbNewLine _

& "Exercise price: " & Format(Exercise, "Currency") & vbNewLine _

& "Risk free rate: " & Format(Rate, "0.0000") & vbNewLine _

& "Volatility (sigma): " & Format(Sigma, "0.0000") & vbNewLine _

& "Time to expiration: " & Format(Time, "0.0000") & vbNewLine & vbNewLine _

& "xlf Input Box demonstrator", , " Financial modeling | excelatfinance.com"

End Sub

When the five parameters have been entered, the line 39 passes the values to the BSCall function procedure in code 2.

Code 2: Function

BSCall displays a series of input boxes as a 5 step wizard. Allows optional default values - returns call price and parameters to a message box

Function BSCall(Stock As Double, Exercise As Double, Rate As Double, Sigma As Double, Time As Double) As Double

Dim d1 As Double, d2 As Double

With Application

d1 = (.Ln(Stock / Exercise) + (Rate + (Sigma ^ 2) / 2) * Time) / (Sigma * Sqr(Time))

d2 = (.Ln(Stock / Exercise) + (Rate - (Sigma ^ 2) / 2) * Time) / (Sigma * Sqr(Time))

BSCall = Stock * .Norm_S_Dist(d1, True) - Exercise * Exp(-Rate * Time) * .Norm_S_Dist(d2, True)

End With

End Function

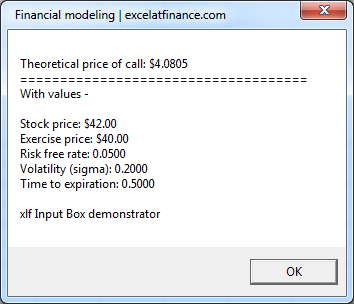

Line 40 to 48 of code 1 then display the message box shown in figure 2.

Related materials

- About the Black-Scholes model

- Coding Box Cancel buttons - with message boxes and input boxes

- This example was developed in Excel 2013 Pro 64 bit.

- Revised: Saturday 25th of February 2023 - 09:37 AM, [Australian Eastern Standard Time (EST)]